| | Ethnic marketing trends | Food waste and retail | Data highlights | Sources | Alberta Food Consumer View home page

,Ethnic Marketing Trends

There are over 200 ethnicities in Canada and Statistics Canada reports that over 70 per cent of all population growth in Canada comes from immigration. By 2017, one in five Canadians will be a visible minority.� ,

What does that mean for retailers?

We found a number of studies on the topic and a few important findings are highlighted here.

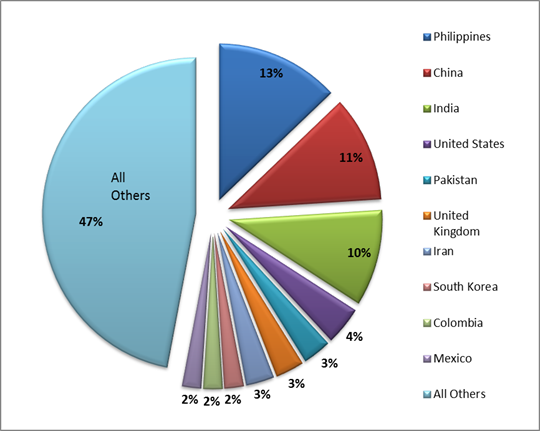

- The two largest visible minority groups in Canada are South Asian and Chinese. The 2011 National Households Survey has South Asian as the larger group, representing 25 per cent of the total visible minorities and 4.8 per cent of Canada’s total population. Chinese make up 21 per cent of the visible minority population and four per cent of the total population (Statistics Canada).

Figure 1 -New Immigrants (2006 to 2011) – Top Ten Countries

Source: Statistics Canada, 2011

- According to Nielsen Research (2015), visible minorities are changing the Canadian landscape. Led by South Asian and Chinese ethnic groups, visible minorities will provide a five billion dollar per year opportunity by 2017 in the retail sector. Some interesting facts about these consumer groups include:

- COSTCO is king: both South Asians and Chinese tend to choose their retailers based on location,

- quality and price. Costco seems to be delivering what they need.

- Snacking is a new behaviour for both groups after coming to Canada: for South Asians “natural” and “not-processed” attributes are important. Therefore, they mostly snack on fruits, vegetable and nuts. They also love spicy and salty snacks found in ethnic stores. Chinese consumers prefer mini-meals. They like warm food and beverages and items that are convenient to make such as dumplings and spring rolls.

- Chinese consumers are moving away from stir-frying towards more healthier food preparations such as baking and steaming.

- Checking labels is crucial for Muslims: buying groceries in Canada is challenging for them as they have to read labels to find out which items are halal.

- Overwhelmed newcomers with busy lifestyles are looking for Home Meal Replacements (HMR) which are fresh and natural.

- Canadian Grocer magazine (2015) states that Canadian big-box retailers are analysing their customer data to understand the multicultural segment. For example:� Loblaw Companies Ltd., using their data has found that -similar to mainstream customers- there is an increasing demand for HMR options and convenience products that are also healthy.� The HRM category is worth $2.4 billion in Canada and within it “multicultural” is the fastest growing segment.�

- Retailers have opportunities to promote multicultural cuisine among non-visible minority consumers as well. Studies have found households with singles and couples are the number one shoppers for multicultural speciality items.

- Smart ethnic retailers are aware of the pockets where ethnic groups tend to live and are quickly building stores in those areas.

- Canadian supermarkets are trying to capture this market by acquiring ethnic grocery stores. Loblaws acquired T&T, the largest Chinese supermarket chain in Canada. Metro has appointed a category manager for ethnic products and has hired an outside agency to help them better understand South Asian consumers.

With over 200 ethnicities in Canada, ethnic marketing is not just a passing fad.� Recognizing these trends are important for retailers, both small independents and big-box. Retailers need to reflect the customers they serve, using� variety of visual, language and ethnic specific media to attract ethnic consumers. Identifying these trends is also important for agri-food manufacturers. Focusing some innovation strategies on products and meal solutions that assist multicultural customers to access healthy and convenient foods could be lucrative.

Food Waste and Retail

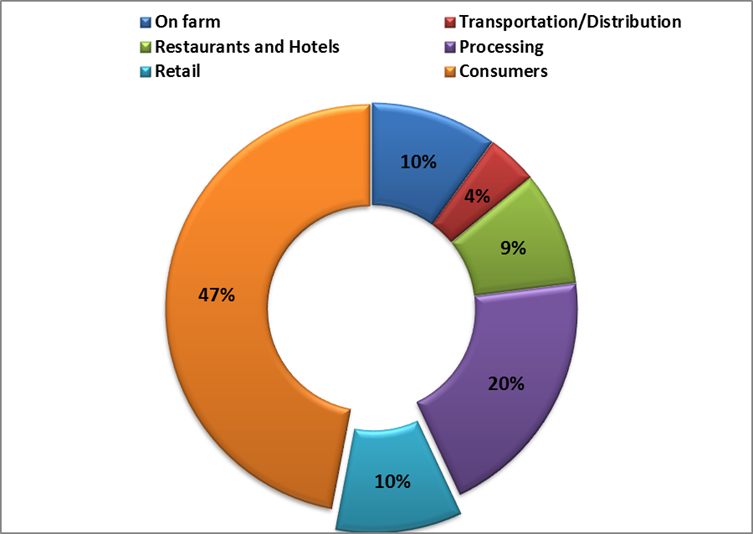

In 2014, the Value Chain Management Centre (VCMC) estimated that $31 billion worth of food finds its way to landfill, compost piles or animal feed each year. The United Nations’ Food and Agriculture Organization (FAO) formula estimates the cost of food waste in Canada would exceeds $100 billion. Figure 2 illustrates where quantifiable food waste occurs along the value chain.

Figure 2: Where Food Waste Occur Through Canada’s Food Value Chain (% Distribution)

Source: Value Chain Management Center Study, 2014

Based on this information, the largest single contributor to waste are consumers. Nearly 50 per cent of the $31 billion in food waste originates from food thrown away in Canadian homes. Total waste at retail level is about 10 per cent.�

Table 1: Hot Spots and Root Causes of Food Waste at Retail Level

What are the hot spots for food waste? | Fruits and Vegetable

Seafood

Meat

Bakery and Deli

Readymade food |

| Why does food waste occur (root causes)? |

Inaccurate forecasting

Food safety issues

Increasing market share of ready-made food

Date codes (expiry dates/best before dates)

Fluctuations in delivery from suppliers

Cold chain deficiencies

Rejection on arrival at distribution centres or store or during handling

Increasing merchandising standards

Product differentiation

Market over-saturation

|

Source: Provision Coalition: Agri-food@Ivey and Value Chain Management Centre

The main way that retailers contribute to food waste is flier promotions. It is found that fliers have the potential to encourage consumers to seek out deals and buy beyond their needs. An almost invariable outcome of this is that consumers place an overly high importance on price and buying in bulk, which then leads to increased waste. The VCMC study indicates waste at retail can be avoided if grocers stopped thinking simply in terms of selling great volumes of products and improve relations along the entire supply chain. The report’s findings also suggest, through reducing food waste, retail business can reduce operating cost by 15 to 20 per cent and increase profitability by about 11 per cent.

Meanwhile,� a number of anti-food waste programs are emerging in Canada and elsewhere. One of the most popular campaigns is called “Love Food Hate Waste” and it was introduced by the Waste and Resource Action Program (WRAP), a charity organization in the UK. Another anti-waste campaign that has received international attention is the "ugly” fruits and vegetable campaign launched by a French grocery chain. It is estimated that this campaign will help to reduce the waste of 300 million tons of produce a year in France. Recently, Metro Vancouver signed an agreement with WRAP to introduce the campaign to Canada with the involvement of other main grocery retailers. Retailers were identified as the most important sector to help promote the anti-food waste message to consumers.

Data Highlights�

Monthly retail trade - Retail sales are down in the first quarter of 2015 compared to the last quarter of 2014. The greatest drop in sales occurred in specialty food outlets and beer & wine stores. Following the holiday season a drop in first quarter sales is considered normal. Stronger sales are expected in the second quarter of 2015.

Grocery Sales in Alberta |

| Quarter 4, 2014 | Quarter 1, 2015 | Percent

Change |

| Supermarkets | $2,793 | $2,517 | �-9.891% |

| Convenience | $173 | $160 | �-7.52% |

| Specialty | $153 | $116 | -24.43% |

| Beer & Wine | $703 | $532 | -24.27% |

Data in millions where applicable.

Source: Statistics Canada, 2015 |

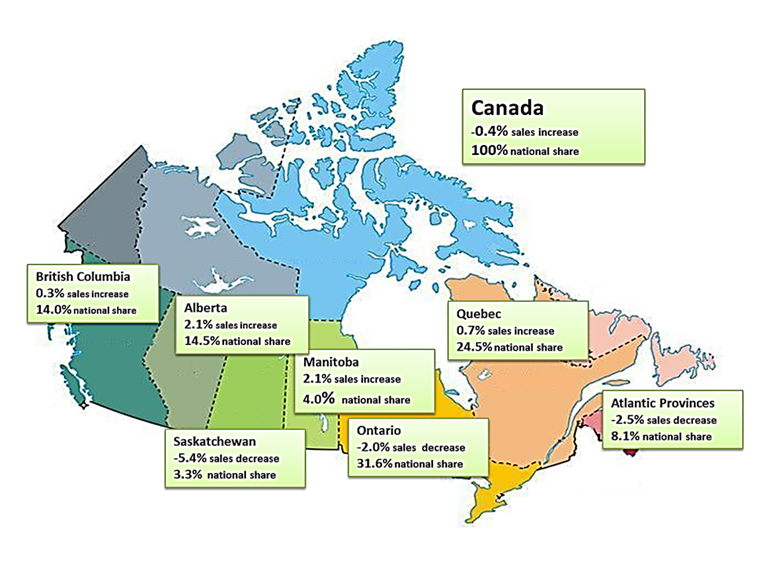

Retail sales growth - Canada 2013

Better than average economy and younger than average population helped propel Alberta’s grocery sales last year. Alberta’s 2.1 per cent increase came on the heels of a 5.3 per cent hike in 2012. Saskatchewan saw the biggest decline last year, while Ontario and Atlantic provinces also show a decline.

Sources:

- Statistics Canada (2011). Immigration and Ethno-cultural Diversity in Canada

- Canadian Grocer (2015). Special Promotional Feature – March/April 2015.

- Fisher, C. (2015). Unveiling Opportunities in Multicultural. Canadian Grocer.

- Nielsen�� (2013). Ethnic Opportunity- If Only I Knew

- Pearl Strategy and Innovation Design Inc. (2013). Understanding the Ethnic Consumer.

- Value Chain Management Centre, (2014, 2010). Food Waste in Canada: Opportunities to increase the competitiveness of Canada’s agri-food sector, while simultaneously improving the environment. George Morris Centre.

- Provision Coalition.� 2013. Developing an Industry Led Approach to Addressing Food Waste in Canada.

- Canadian Grocer. Various Issues

Trends in Retail - Issue 2 - pdf copy

|

|