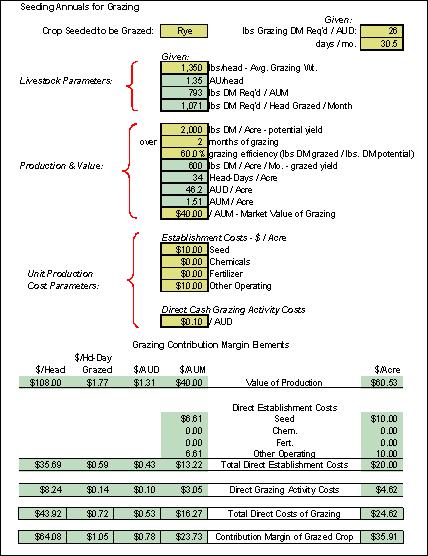

| | Given a situation where your existing crop is essentially written-off, direct seeding an annual cereal for later season grazing is an option. The objective is to replace drylot feeding days later in the season.

.A direct cash cost budget, as presented on this page, builds in a number of the key considerations in pursuing this option. The major assumptions underlying this budget include:

- Soil moisture conditions are sufficient to achieve germination and growth

- Cereals are direct seeded into existing crop land at a custom rate of $10/acre (reasonably reflective of the cash costs of doing the seeding yourself)

- Chemical and fertilizer inputs are specifically excluded - for cash flow reasons, reduced likelihood of benefit to their application, plus some expected carryover from the original crop

- The potential yield over a two-month window is penciled in at 2,000 lbs. of dry matter per acre. At a grazing efficiency rate of 60%, this works out to a grazable yield of 600 lbs of dry matter per acre per month, or 46.2 Animal Unit Days (AUD) per acre

- Direct cash grazing activity costs are estimated at $0.10 per AUD, including a nominal amount for feed supplements as required. This estimate does not include a valuation of operator labour used to manage the grazing activity (which can effectively double this cost)

- A $40/AUM market value of grazing is used to reflect the value side of the budget. Depending on your locale, this amount may, or may not, seem realistic. The sensitivity table on the next page provides cash break-evens over a range of market rates.

Focusing on a cash items only, at the assumed rates and costs, direct cash costs associated with laying in the additional grazing days tally to $24.62 / acre, or $16.27 / AUM. The cash margin, incorporating a market value for the grazing, works out to $35.91/acre, or $23.73/AUM.

The purposes of the cash budget were:

- To determine whether or not this option would pencil out on a cash basis, as a short term measure to lay in grazing head-days, and

- To lay out costing elements to be included in the overall cash flow for your farm.

The margins, in essence, reflect the net cash benefit over renting grazing at the posted rate. They represent the amount remaining to cover operator labour and other overhead costs.

From an agronomy perspective, a few production management considerations include:

- Seed a mixture of spring cereals and winter cereals (seeding rate of 90 lbs/acre of winter cereal along with a bushel of oats or barley),

- This seed mixture will take advantage of the quick growth of the spring cereals, but will allow for the regrowth provided by the winter cereals along with their ability to continue growth after fall frosts, and

- Rotationally graze these annuals to reduce wastage and increase grazing efficiency.

Further detail on grazing cereal crops in available in the Alberta Agriculture Agri-Facts publication “Winter Cereals for Pasture” (1) Agdex 133/20-1.

Given reasonable growing conditions, this approach should optimize the number of “days” you can re-coup from your acreage.

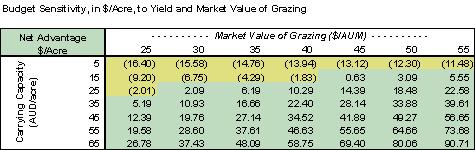

The final consideration in assessing this option is the potential down-side risk, particularly as related to yield. The “budget sensitivity” table shows the net cash margin under different yield and grazing value scenarios. Realistically, yields need to be in the 20 AUD / acre range to have this “seed and graze” option work.

For more information contact:

Alberta Ag-Info Centre at 310-FARM (3276) |

|