| |

In 2016, the Farmers’ Advocate Office (FAO) received several inquiries from freehold mineral owners who were being approached by Alberta Energy for the payment of outstanding freehold mineral tax.

A freehold mineral lease will typically establish an arrangement between the company and the freehold owner for the payment of taxes. The exact nature of this agreement will differ from contract to contract. The freehold mineral tax is based on production of the asset.

Freehold owners should be aware that, notwithstanding anything in the lease agreement, they are ultimately responsible for the payment of the freehold mineral tax under the Freehold Mineral Taxation Act if the company becomes insolvent or refuses to pay.

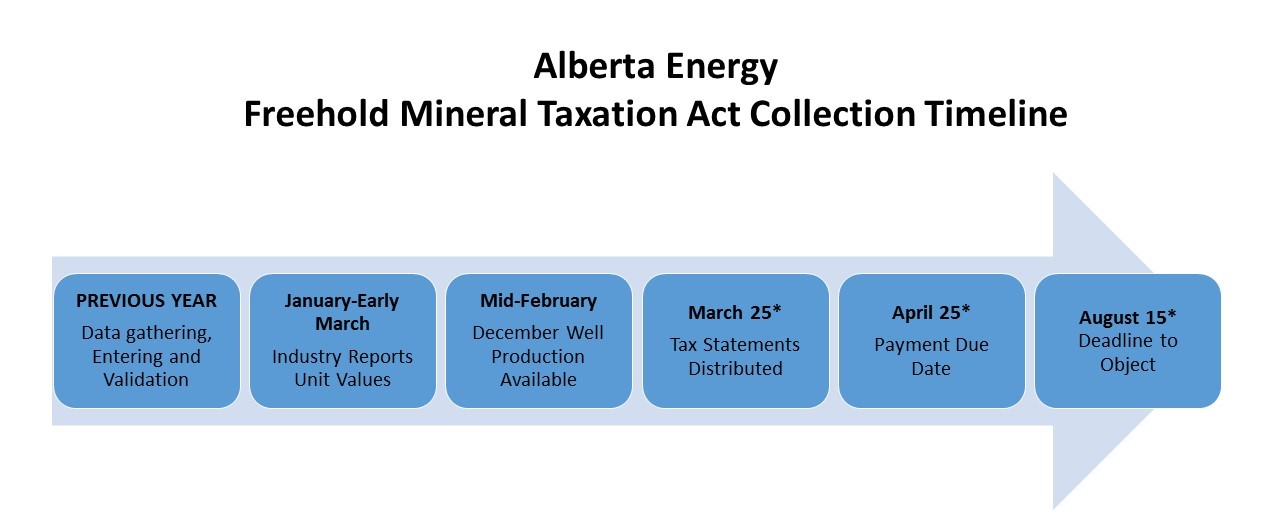

Freehold minerals have been subject to some form of provincial production tax since 1938. The current Freehold Mineral Taxation Act was established in 1983. The legislation allows that if collection efforts with the designated payer are unsuccessful, the Crown may approach the freehold owner for payment of the outstanding amount. Under the Act, the Crown has the ability to revoke freehold mineral title if these amounts are not paid. To date, this action has never been exercised.

Since the tax is based on production, the amount owing will vary depending on what production was reported during the previous calendar year. On average, the amount of tax levied is 4% of revenues reported from freehold properties. Many low-producing wells are exempted if the total tax is less than $1,600. In 2015, the Crown collected $84 million in freehold mineral tax. In the vast majority of cases, the tax is successfully collected from the designated payer, but freehold owners should be aware of and plan for this risk.

If you have questions about the freehold mineral tax, please contact Alberta Energy 780-427-6000 or e-mail: MinTax.energy@gov.ab.ca. |

|