| | The New Current Liabilities section at the bottom of the Cur-Liab page allows for the entry of new current liabilities projected to come in during the time period in the projection. For example, if the year runs January 1, 2015 to December 31, 2015 and it is expected that a grain advance for say $100,000 is going to be taken out October 15, 2015, that entry can be made in this section, and the $100,000 will then come into projected cash flow in October of the year. This section allows for only one payment (amount and date) to be entered however, so if more than one payment on the debt is anticipated in this projected time period (say $25,000 November 15, 2015 and say $35,000 December 15, 2015 for example), both those planned payments cannot be reflected for that entry.

.

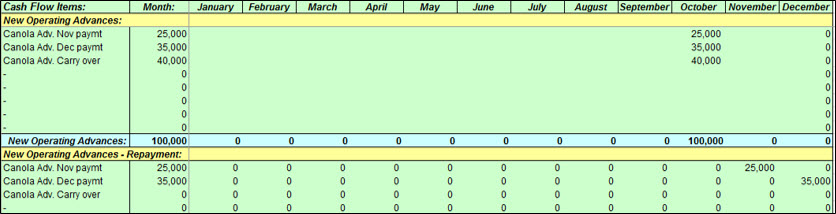

If it is expected that more than one payment will be made on a new current liability, an easy way of dealing with it is to break the debt down into parts reflecting how repayment is anticipated, and then showing the payments accordingly on each. For the new current liability described above, the new advance could be broken down into three entries. The first would be for $25,000 to be taken out October 15, 2015, and then fully repaid November 15, 2015. The second would be for $35,000 again taken out October 15, 2015, and then fully repaid December 15, 2015. The last would be for $40,000, and no payments or payment dates would be entered. ABA would then carry that portion of the debt over to the year end. Alternatively, two entries could be made – the first as described above, and the second for $75,000 with one payment of $35,000 December 15. In that case, the residual amount of the second loan, not repaid, would be carried over to year end. For clarity however, if the debt is going to be split as in this example, it is suggested it be done as first suggested. An illustration using this example is shown below:

The cash flow resulting from this new projected liability would be as per the Op Advances page, shown as follows:

|

|